The next four years could be a bit awkward especially for new readers. One might assume that I applaud the Trump Presidency but my political and social views are of secondary concern. My role is to interpret the direction and behavior of policies and markets and hopefully be on target.

Quick Summary of 2016: One year ago our base case scenario was the economy and markets were rolling over into recession and that downside risk of stocks was much greater than the potential upside. This proved to be the correct assumption as many categories of stocks (especially Value stocks) were in full-fledged bear markets. We avoided a sharp 15% decline in January-March and the Brexit decline in July. During the April-May period forward looking economic data began to improve sharply and the recession was avoided (first time for such a turnaround since 1985). While I deeply regret lagging the major indices in performance this year, the risk/reward last Spring was disproportionally negative and preservation of principal is always my #1 priority. 2016 will represent an economic mid-cycle bottom which supports the prospects of acceleration in 2017.

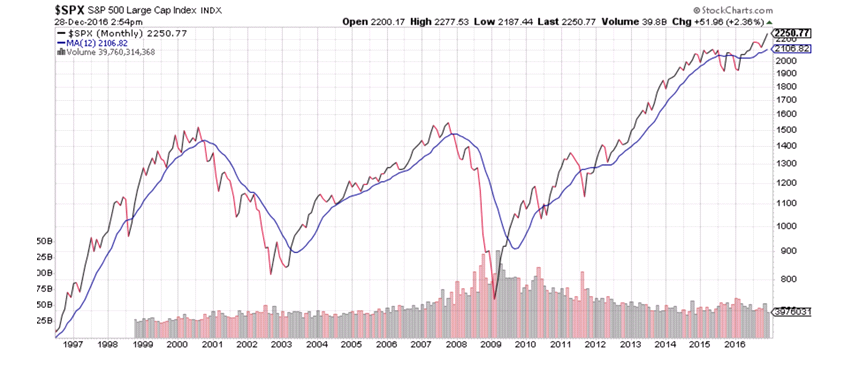

Below is a basic trend model which uses the 12 month moving average (ma) of the S&P 500. When the SPX is above the 12 month ma the trend is bullish/positive. Moves below the 12 month ma indicate a potential change in trend and a time for caution. It’s not perfect but when combined with an eroding economy the results can be devastating to the Buy and Hold investor not paying attention.

And then there was the election……

We’ve now had just over a month and a half since the election during which the fundamental approach to fiscal and monetary policy had been turned upside down.

If Hillary Clinton was elected last month with Republicans maintaining control of the House and Senate would have represented maintaining the status quo regarding the use of monetary policy as the only tool to defend against the next recession. This implied that the US would likely have gone to 0% or less interest rates when the next recession occurred. A powerful fiscal stimulus plan was out of the question with Republicans control of Congress. This implied that we were staring at the next 8 years believing the odds of recession were high but policy response was restricted to whatever the Federal Reserve could accomplish as it was the only tool available. Given that interest rates were already very low, the possibility of negative rates was real.

Since the election this perception has monumentally changed. It’s now obvious that any future recession will now be met with both Monetary stimulus and a huge Fiscal stimulus package. Markets are smart enough to know the only reason Republicans opposed a Fiscal stimulus plan was that a Democrat was in the White House. While DT may laud himself for this change in perception it’s likely that it would have happened with any Republican winning the Presidency. It’s my belief that this premise caused Treasury prices to plummet in one of the worst 30 day periods since 1980 and for stocks to spike higher.

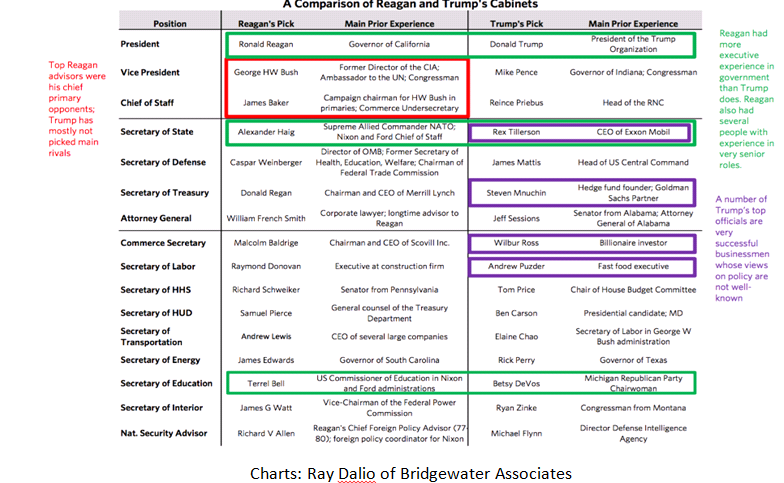

With the addition of the cabinet picks it’s becoming obvious that there we’ll experience a profound ideological shift led by a President who loves to negotiate hard and doesn’t mind being the bull in a china shop. It appears his cabinet is being filled with those hell-bent on making big changes in policy primarily in reversing many of the post-2008 reforms. This shift in attitude and direction reminds me a great deal of the transition from the Carter to Reagan Administrations where we went from a low growth/cautionary Presidency to an Ayn Rand influenced direction.

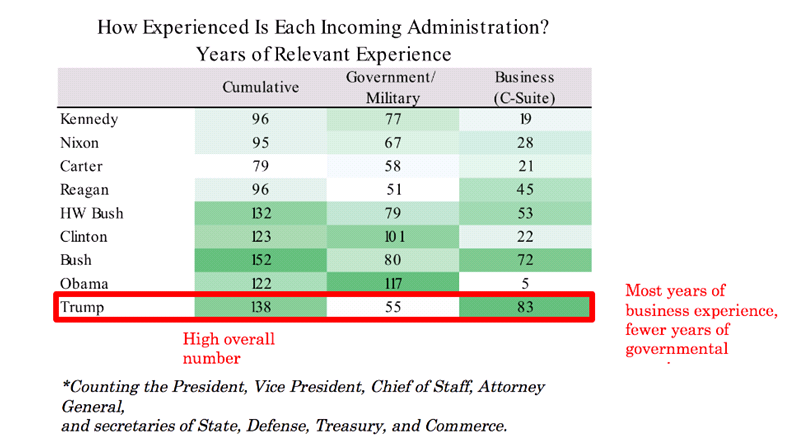

Trump’s cabinet is a reflection of his business perspective and the direction he wants to take the country. The chart below shows the business/government experience of his top 8 picks in cabinet. By far, Trump has assembled a cabinet with the greatest amount of business experience and it’s my expectation that this is a business first administration.

While the final policy drafts remain to be seen the impact on the US economy, the potential shifts in tax and fiscal policies alone could create a virtuous shift as money comes out of cash to risk oriented investments. Money always tends to be attracted to places where it’s well treated. A pro-business administration with the rule of law and political stability would offer a very attractive landing spot for foreign capital.

What could go wrong?

Since Donald Trump’s ego is on continual display my belief is that he does not want to be remembered as a Presidential failure but it won’t be easy. Abandoning environmental, the ACA, social progress, immigration and avoiding the real driving issue of under-employment (Robotic Automation) leaves him very vulnerable. His political platform on employment is detached from the reality of advancing productivity via technology.

In addition Trump lost the popular vote by close to 3 million and has the lowest approval rank of a new president in recent time. Add to this a popular (60%+ approval), eloquent and young former President to play the role of Devil’s Advocate with preservation of progress in mind.

Of course, one has to wonder if the incoming administration and cabinet will not only just be aggressive but will they be thoughtfully aggressive?

All these potential pro-growth initiatives would have you believe that unemployment is high but employment is not high, it’s 4.6%. At 5% or less is about the level where historically the Federal Reserve will begin to raise short term interest which will have a dampening effect on the economy to lower the risk of inflation.

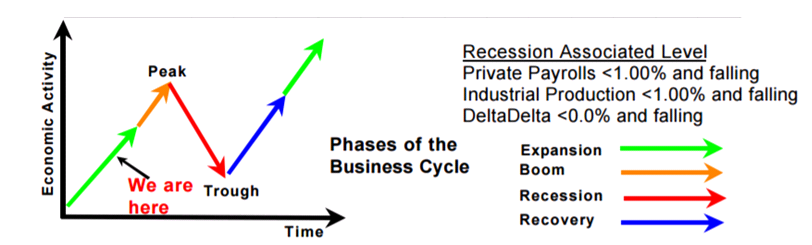

Many times over the years I’ve mentioned Bob Diehl of Nospinforecast.com and his documentation of the business cycle. According to Bob from the chart below we are approaching the “Boom” phase of the economy where employment really starts to tighten and the Fed gets quite aggressive putting on the brakes. My sense is that Trumps policies will likely ignite the Boom phase and result in a battle with the Fed unless Trump can replace the inflation hawks on the Fed Board when most are up for re-appointment in 2018. Even if Trump does replace the Fed board he could ignite a significant hike in inflation.

Odds are quite high that Trump will have to deal with a recession at some point, especially if he serves an 8-year term. How will he cope with that given the sky-high expectations he has created for his presidency?

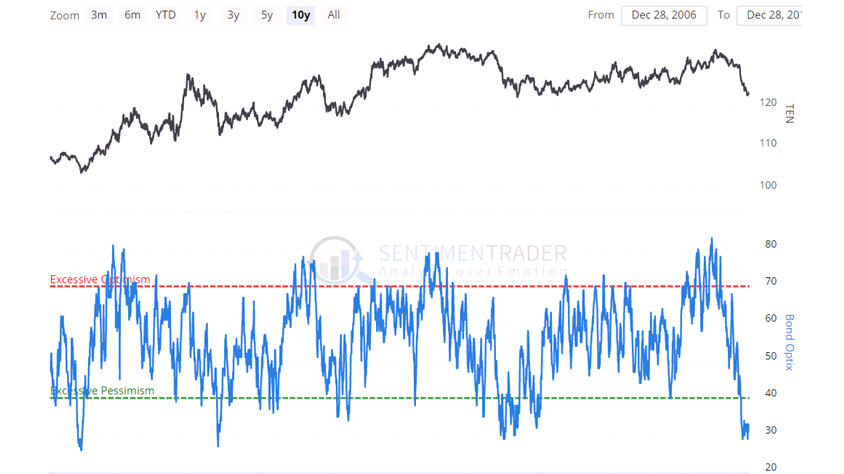

Balancing Trump risk with Treasuries, Utilities and REIT’s: The surge in stocks came at the expense of bonds and it appears that Treasuries are putting in a bottom, at minimum the risk after the decline may not be much at all. Investor sentiment for bonds is the polar opposite of stocks which means extremely negative and so much of the risk is likely washed out for now.

Below is the TLT which is the 20-30 year Treasury ETF at $118 might now be suitable for intermediate to long term investors. This is the same holding we sold 20 points higher at $137 to $139.

The broad sell off in bonds has created what could be an excellent long term entry point for interest rate sensitive investments such as water utilities and real estate investment trusts.

Investment selection for the new administration: The Return of Value hedged with interest rate sensitive holdings

Had HRC won the election there would have been no pivot to Value oriented stocks and strategies at the expense of traditional growth stocks especially Tech stocks.

In addition, with the prospects of a Fiscal package coming in the next year or two beaten down Value stocks and Value strategies have come back to life. Value generally doesn’t do well when a recession is looming but Value is also the place you want to be when economic cycles bottoms as it has this year.

The graph above highlights the relative performance of Value stocks compared to Growth stocks. Value did very well from 2001 to 2007 but has lagged since 2007 with the exception of 2012/2013. With the business/economic cycle making a bottom in early 2016 we can see a turnaround to Value is now in play.

Just after the election I returned to using the investment selection factors that have proven time and again to be the most effective when Value is performing well. Plus, the Growth stocks that we own or will be purchased in the near future are in long term uptrends lasting multiple years. The pullback in Growth stocks does provide a good entry point for Amazon, Equinix, American Water, Equity Lifestyle Properties. In addition, with the understanding that this move out of the 2-year go-nowhere trading range raised the odds that this rally is part of a multi-year up move in stocks. Most of the new additions were selected with potential for long term holding periods of hopefully a year or more.

The post-election surge came primarily at the expense of bonds and interest rate sensitive holdings which were hit extremely hard. These are the types of investments that would likely do well in a slowing economy.

Considering that there is no assurance that Trump will be able to realize his economic predictions and that it’s very likely the Federal Reserve will keep raising short term interest rates there is no guarantee of the long term success of his plans especially if Republicans lose mid-term elections in 2018. Hence, the selloff in bonds and interest rate sensitive stocks makes sense given the steep selloff they’ve already incurred.

No doubt you’ll see all sorts of predictions for investment markets for 2017. Pay them zero attention as no one really ever knows what will happen in the future. Most strategists have to always be positive on markets to reinforce their brokerage force to buy stocks. Generally speaking trendlines are amongst the best tools to determine whether to be invested in stocks or not. Trendlines are price driven and

objective with no opinions to taint their perspective. In addition just by following basic trendlines like the 200 day moving average will generate returns and reduce downside risk better than any guru or strategist. While trendlines were quite negative for most of late 2015 and early 2016 they are very positive for the time being.

Have a great 2017 everyone!

Brad Pappas