Stocks remain in an uptrend. For the first half of the year Tech stocks were the dominant sector. Since the Fed shift in June Healthcare and Finance have joined Tech in leadership. June witnessed a pullback in prices for the market leaders of which we owned many. This short pullback bottomed on the last day of June. Since June 30th most accounts are up at least 3%

No major economic risks at the moment for at least a year or two. While I expect some economic slowing in the second half of the year due to Fed rate hikes, slow growth doesn’t equate to Recession. The ingredients for a major business cycle top are still absent.

Last week I spoke with Bob Dieli of Nospinforecast.com regarding the present status of the economy within the larger business cycle. My concerns were due to the rate hikes and low unemployment and might these be signs of final “boom phase” of the economy. His answer surprised me:

Me: “If this was a baseball game what inning do you think we’re in regarding the economic expansion, the 7th or 8th?”

Bob: “I would say more like the 6th. The reason is that I don’t think the early stages of this expansion used up resources at the same pace as other long-lived episodes. We have yet to see any serious adjustment in interest rates, and we have yet to see even the slightest hint of wage pressures. Both of those are 7th and 8th inning types of events.”

“Of course, the one thing that you did not mention is the weather. A cloud burst, say in the form a failure to pass a debt ceiling bill, or some strange action by the FOMC with the balance sheet, or the Europeans getting their shorts in a knot yet again, could bring an end to the game before the 9th inning.”

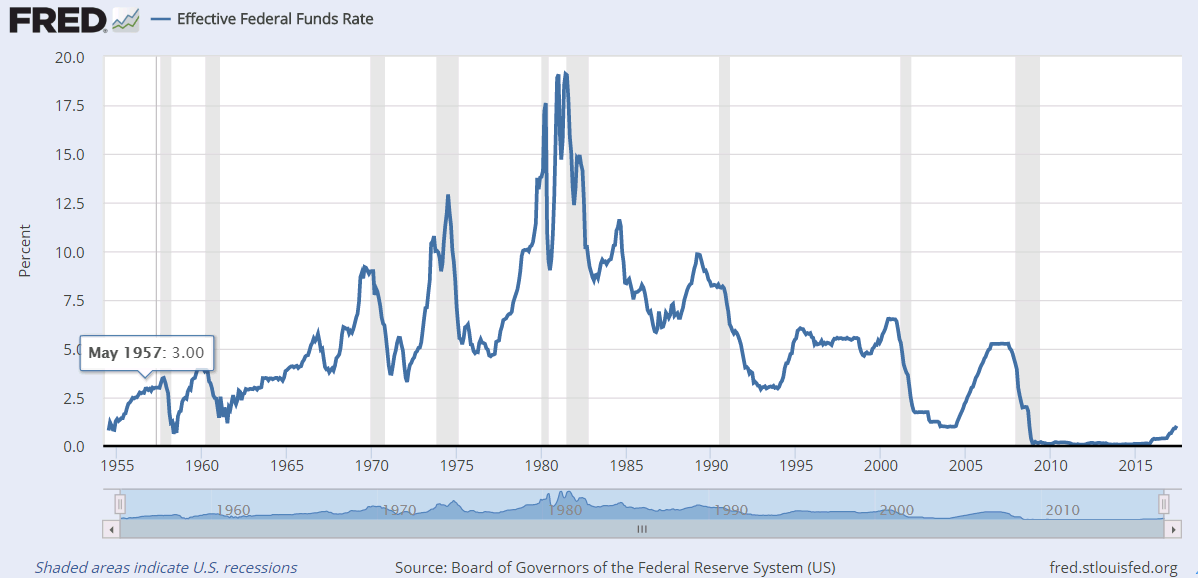

Interest Rates Rising: For 9 years the Federal Reserve has been pushing down long term interest rates by being heavy buyers of long term Treasury bonds. In May, based on the price trends in Treasury bonds I began to take some of our losing/lagging stocks and shift the proceeds to long term Treasuries. This was based on the price action trend and the potentially serious implication of the Yield Curve narrowing – see chart below. But, Janet Yellen at the Fed admitted she pays close attention to the Yield Curve too and announced the Fed will no longer be buying bonds but in fact selling bonds which put an end to the rally in Treasuries. This caused a sharp pullback in bond prices which triggered our sales which are always present to keep losses to a minimum.

So are at the end of a nine year cycle of continual downward pressure on interest rates? If you’re looking to lock in a rate on a mortgage this may be a good time to do so.

With the Fed selling bonds in the open market they will probably cause interest rates to gradually rise while reducing the money supply. (They sell the bond and the buyer gives them cash taking the cash out of the system) This does represent a potential headwind for stocks. However, central bankers will try to balance the sale of debt and interest rate hikes to keep growth and inflation neither too hot nor too cold. But eventually they’ll go too far and then we’ll have our next economic downturn. But according to Bob Dieli, don’t look for the downturn anytime soon.

Money, Markets and Murder

From the title you may think this months newsletter has more to do with Agatha Christie than markets will be disappointed. While I’m more of a Philip Kerr fan this letter will make reference to a case of repeating cycles and the serial murder of economic expansions.

The two biggest questions I receive revolve between “How can the keep rallying with the chaos and ineptitude in the White House?” and “How much longer till the next recession?”

The last letter I wrote analyzed the US stock market from a Technical view point in which I used various moving averages to identify major turning points in the market indices. The technical view of the markets is really the latter half of the “cause and effect” duo. Market reactions are the effect and in this letter I’d like to address the “cause”.

Markets and economies don’t roll over randomly. To quote the German economist Rudiger Dornbusch: “US economic expansions don’t die of old age. Every one of them was murdered by the Federal Reserve.”

Well now……….That may seem to be just colorful language but the continual coincidental circumstances of should dispel anyone thinking its just a mere coincidence.

The tightening of credit or raising short term interest rates is on the short list of weapons of choice for the Federal Reserve. Perhaps the evidence is strictly coincidental but we have a repeating circumstance that just so happens to be at the scene of every “murder”.

One does not have to be Hercule Poirot to see that a rising Fed Funds rate is seen before every major recession since 1954. Short term interest rates do not rise on their own accord. The Fed’s Open Market Committee pegs the rate in accordance with how they view employment and future growth. No magnifying glass is needed to see that sharp rises in short term interest rates are closely followed by economic slumps.

While investors have no control over short term interest rates investors do have control in the open market via supply and demand with long term interest rates. Normally long term interest rates are higher than short term rates. If a 30 year Treasury bond yields 4% and the one year Treasury bill is 1% we would say it has a positive spread and slope of 3%. The actual numbers change on a daily basis but the Trend is the most important factor to consider.

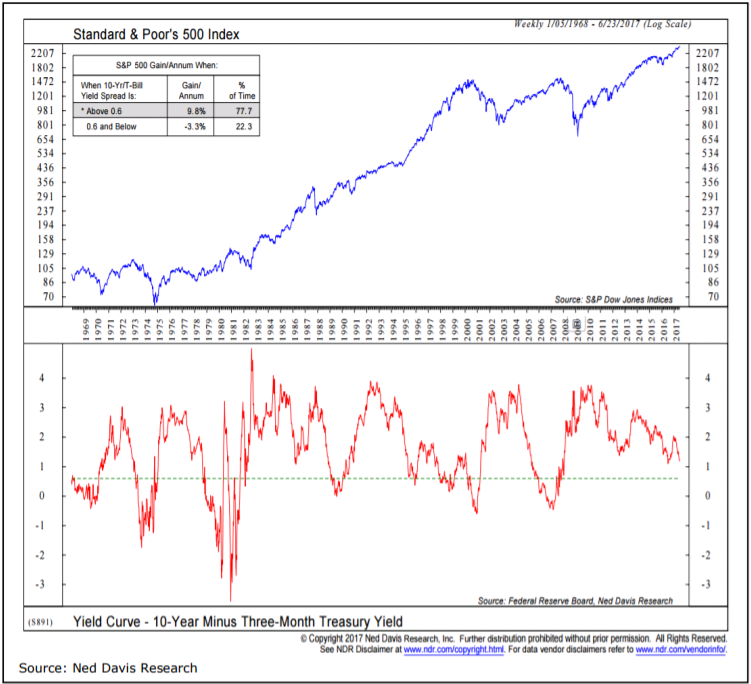

The chart below from Ned Davis shows the performance of US stocks based on the yield curve. They use a threshold of .6%. For example if a T-Bill rate is 1% the yield on the 10-year Treasury bond would have to be equal or below 1.6% to create a spread of .6%

According to the chart above when the spread is above .6% the gain per annum for stocks is 9.8% annually. Below .6% reveals a loss of -3.3% annualized. This doesn’t even take into effect the severe draw downs in account values or the increased volatility and risk, sleepless nights, higher blood pressure and visits to the Astrologer.

This is one of the biggest cons played on regular retail investors by mutual fund companies (especially Index funds and Robo’s) and financial professionals who tell investors that “markets can’t be timed” “you should buy and hold” or “you’re in this for the long haul” when they’re down 30%. This is because the fund companies get paid more to have you invested in their mutual funds rather than in cash or a money market account. I also know a several financial planners who’s “specialty” is reducing taxes on a portfolio. While that may sound good, at the same time their “buy and hold” philosophy means major losses in principal.

While it’s next to impossible to consistently “time” the market in the short term it’s very possible and wise to construct your investments in accordance with US monetary policy which is long term oriented.

I hope everyone has a great Summer.

Cheers,

Brad Pappas

970-222-2592 direct

720-310-8056 Skype

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Past performance is no guarantee of future results.