“The Federal Reserve…is in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up”.Fed Chair William McChesney Martin 1955.

“I think we are actually at the point of encouraging risk-taking and that should give us pause. Investors really do understand now that we will be there to prevent serious losses.” Fed Chair Powell in 2012.

“If the Dow Joans ever falls more than 1000 “points” in a Single Day, the sitting president should be “loaded” into a very big cannon and Shot into the sun at TREMENDOUS SPEED! No excuses!” DJT tweet, February 25, 2015, 12:27am

Any wonder why we seem to have more risk asset bubbles these days?

Quick Summary

Stocks: Stocks have have made a stunning rebound from a near-death experience last year and continue to trend higher. On any market weakness, the White House continues to trumpet a near and close China trade deal. In addition, the economy has turned modestly up again which provides a positive back drop for stocks. My guess is there is a selloff looming as the current rally is losing steam. But the Fed will likely step in and lower rates if a selloff occurs, so the decline would be worth buying.

Fed Policy: The Fed has done a complete 180 turn which provided positive stimulus to both markets and the economy. Much of this has been done at the expense of Fed credibility.

Considering the public pressure being imposed by the President both in public statements and Fed board nominees, we do have to wonder how unbiased they really are.

DJT’s preference to stuff the board with sycophants is troubling but there has been stiff resistance to Cain and Moore. Kudlow’s claim that they’ll never hike rates again in his lifetime is just as bad. Investors may feel invincible with the mistaken belief that the Fed will bail them out from future declines.

The bottom line IMO is the Fed being willing to risk their creation of another asset bubble in the hopes of extending the economic expansion is irresponsible. Our expanding deficits will never be paid off either. Eventually this view will be inflationary wherein the dollar has little meaning and makes a case for Gold longer term.

Economy: After last years series of ugly macro data, a Spring rebound led by employment and housing is underway. A recession starting in 2019 doesn’t appear likely. This is similar to what we experienced in 2015 and 2016.

Treasury Bonds: Since we’re not facing a recession in the near to medium term, the rationale for owning Treasury bonds diminishes. Bonds will likely be a drag on returns and holding uninvested cash in money markets is likely a better alternative.

The bearish argument for bonds is MMT otherwise known as Modern Monetary Theory. Simply stated, MMT is the federal government printing of new money to fund governmental expenditures. One of the risks is a significant increase in inflation. More to come.

Despite the market strength from the late December lows it has been a frustrating period for an investor who uses the past as a guide to the future. While we did manage to keep losses minor in the September to December selloff, we have not nearly kept up with the resulting rally.

The Fed and other Central banks stepped in to halt the decline by easing their monetary stance. Markets should be allowed to trade without continual interference from the Fed since occasional purges are necessary to avoid – otherwise the Fed will create a much larger asset bubble.

There’s no way to ever be sure where the market will bottom, especially when selling gets as emotional as it was last year. As I’ve mentioned several times, V-shaped market rebounds are generally a low probability since 3/4 of all market selloff’s retest the recent low in a matter of days or weeks. For example, from the chart below, the January 2018 selloff retested the lows 3 times. The precipitous decline late last year did not retest even once, which left us too cautious when we should have been much more aggressive.

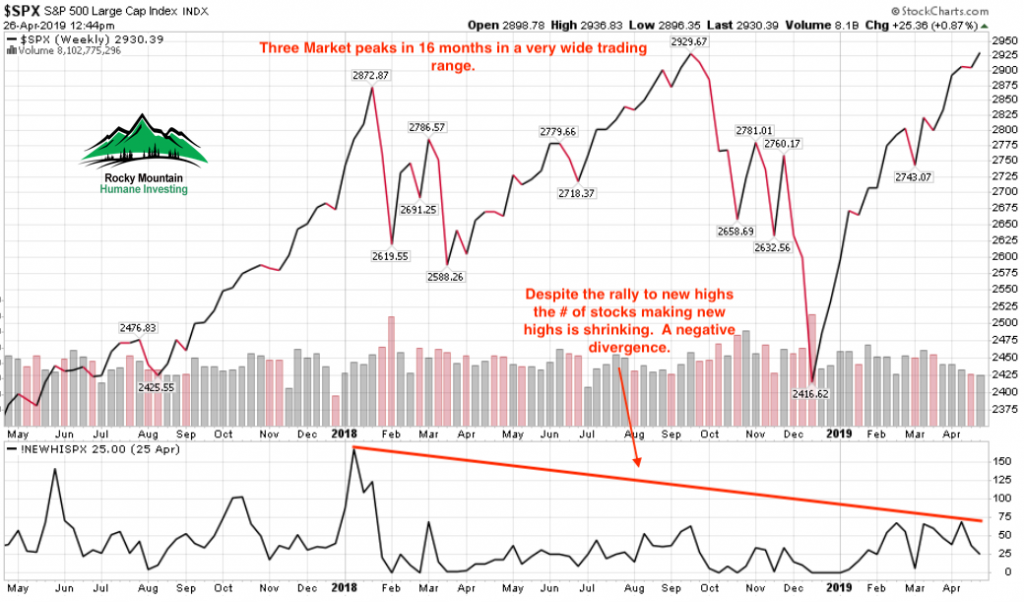

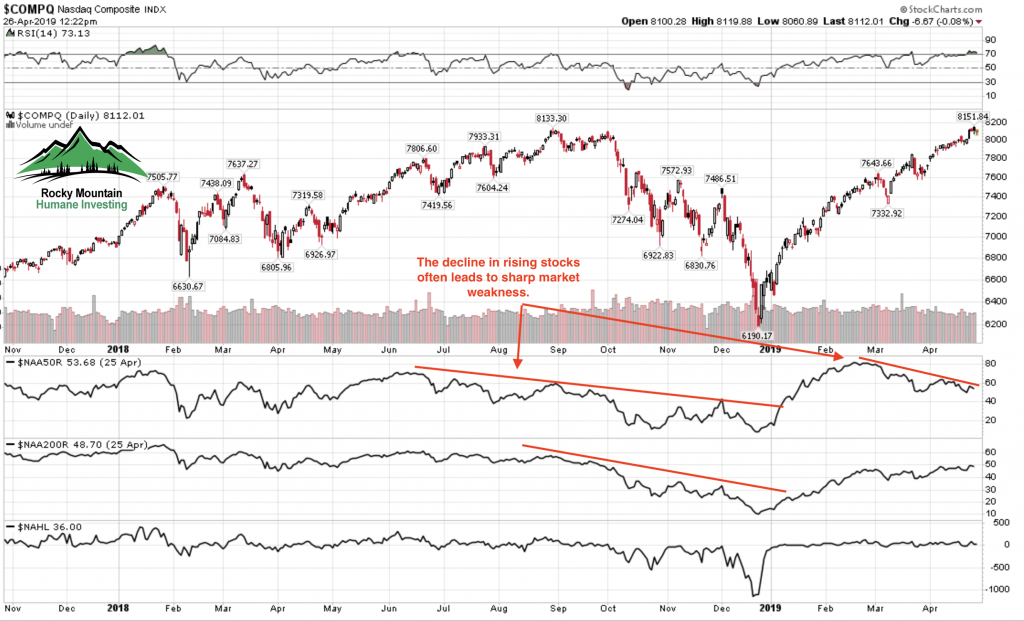

In addition, despite the new highs in the indices, there is erosion below the surface. The number of stocks participating in this rally in the Nasdaq is declining. When I see this kind of erosion in participating stocks, I prefer to hold higher than average amounts of cash in lieu of trying to force the issue. Early warning industries like semiconductors, such as previously held Xilinx and Nvidia, have issued warnings of declining sales which means the underlying global economy is not good. Even Amazon, which reported great earnings and continues to grab market share, is seeing the slowdown as well.

Fewer stocks are holding above their moving averages, revealing a weakening rally and likely selloff.

In addition, the number of stocks making new highs is shrinking fast. These are signs of an old tired market that needs a pullback. In my experience, this is a time to have high cash levels rather than increasing stock exposure.

And then there’s this…..

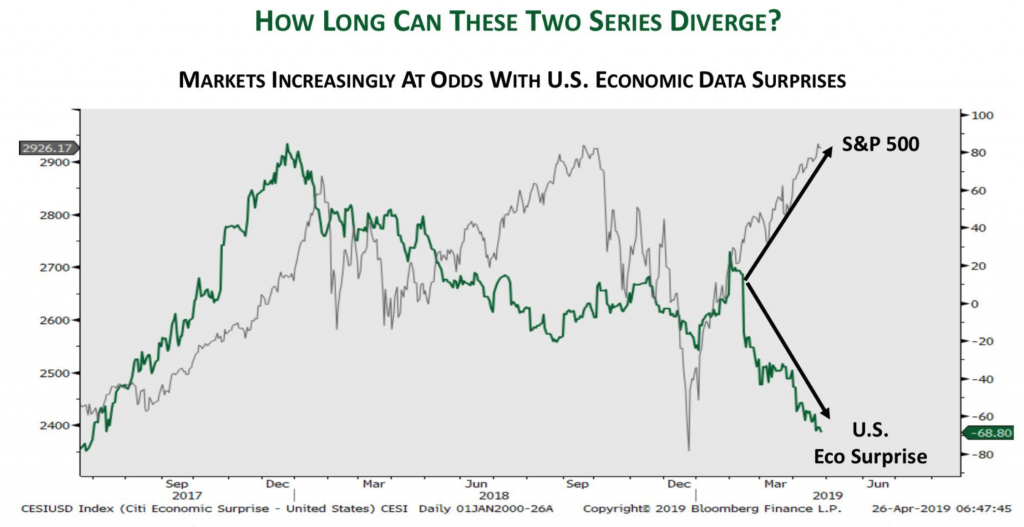

Stocks tend to move in sync with economic surprises. The current gap is due to the significant rally in stocks while the economy has been slowing. Something has to give eventually. Either data turns up or stocks come down or meet in the middle.

The first four months of the year have been the most challenging for myself in years. I read today that this year’s rally is the strongest since 1987. And, the commentators say that without irony or dare mention what happened in the second half of 1987. If you’re unaware, it fell 22.61% in a single day (October 19, 1987).

The presidential administration isn’t even trying to hide the fact they’re manipulating markets to their political advantage. If it isn’t the “trade negotiation are going really well” ad nauseam before markets open or middle of the day on a down market day. Or, Mike Pence: “The economy is roaring. This is exactly the time not only to not raise interest rates, but we ought to consider cutting them.” This is blatant and so wrong-headed it staggers me. This should be the time for the Fed to slowly raise rates so they’ll have firepower to fight the next recession.

Does this mean the time to raise rates is in a recession?

But this is all about the next election, to keep a very old economic expansion alive thru 2020 to get re-elected. In their eyes, market selloffs are merely “glitches” which they take no responsibility for because, in their eyes, markets are meant to only go higher, never lower.

Investors not paying attention will eventually get badly burned. Mean Reversion is one most reliable investing concepts there is. From tulips and bitcoin, to stocks and real estate, all bubbles eventually end. The end is always fast especially for those unaware.

Despite my expressed negativity I’m not calling for a bear market at present. Investor sentiment is extremely positive (which is not good) and similar to what we saw last January before markets sold off quick and deep. But any serious weakness will likely be met by Central Bank easing or cuts by our own Fed. So I think any dip is buyable.

As for where we are currently: We are now entering the most difficult 6 month period for stocks and rather than try to make up our lagging year-to-date performance by increasing risk, I prefer to wait for a decline. Eventually even in this endless market advance a “glitch” has to be looming somewhere.

Quick Summary: The end of an era may be at hand. The rally in bond prices that dates back to 1981 appears to be over. I’m not convinced it’s over for good but that’s an argument to be made later on.

In the meantime, falling bond prices represent a headwind for stocks and could remain so until bond prices find a short term floor. This headwind accelerated the decline in stocks on October 4th and 5th. This prompted me to raise cash from holdings that either had losses or were laggard holdings. A portion of cash was used to purchase hedges to offset any future stock price declines.

It’s most likely that this is just a short or intermediate termed decline in stocks as the long term trend remains firmly in place. Part of the purpose of quick market declines is to make investors fearful and uneasy, one reason we use hedges to cushion declines.

Chart 1: This chart below shows that the long term trend to lower interest rates is being threatened. This can’t be a surprise with the rapidly expanding deficits and very low unemployment. But as I’ve highlighted with arrows: it’s not uncommon for interest rates to rise in the latter stages of the business cycle, only to fall hard when the Fed raises rates enough to trigger recession. I don’t see this time as any different. My best guess is the current bond weakness is a future buying opportunity later in 2019.

Chart 2: Proxy for the 30-Year T-bond is the TLT. The chart below is inverse to Chart 1 above. Any further weakness with a close below $113 could accelerate the bond sell-off which would trigger more stock market weakness in the short term.

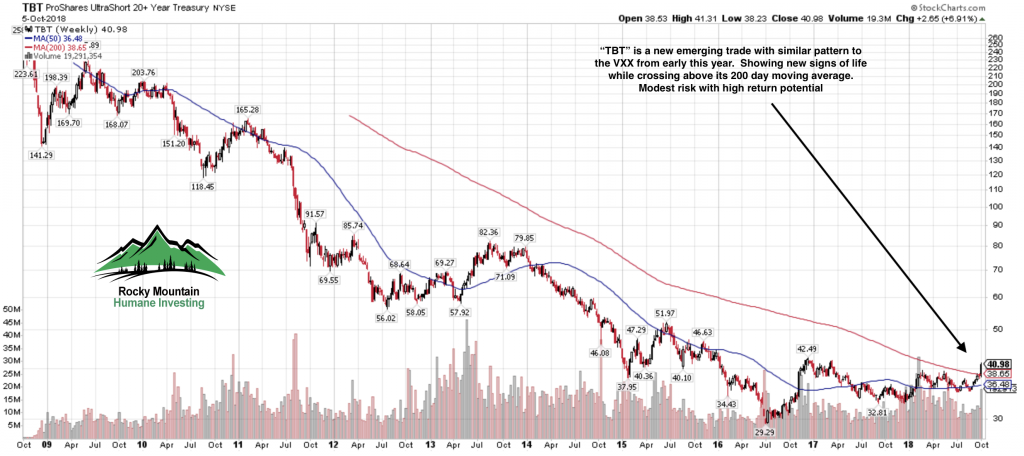

Chart 3: A direct beneficiary of the decline in bond prices is setting itself up for a very good risk/reward trade. As the bond market declines, the TBT will rally higher.

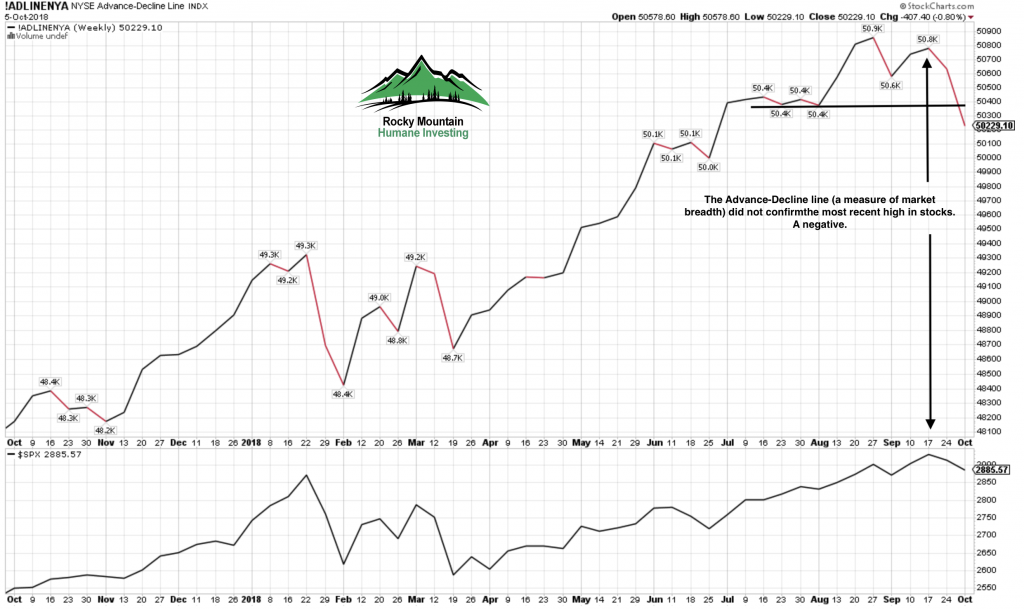

Chart 4: Internal market strength was showing an important discrepancy with the Advance/Decline line which did not confirm the most recent market peak as it should. This non-confirmation gives us a clue that internally at present the stock market is not very healthy and is in need of a purge.

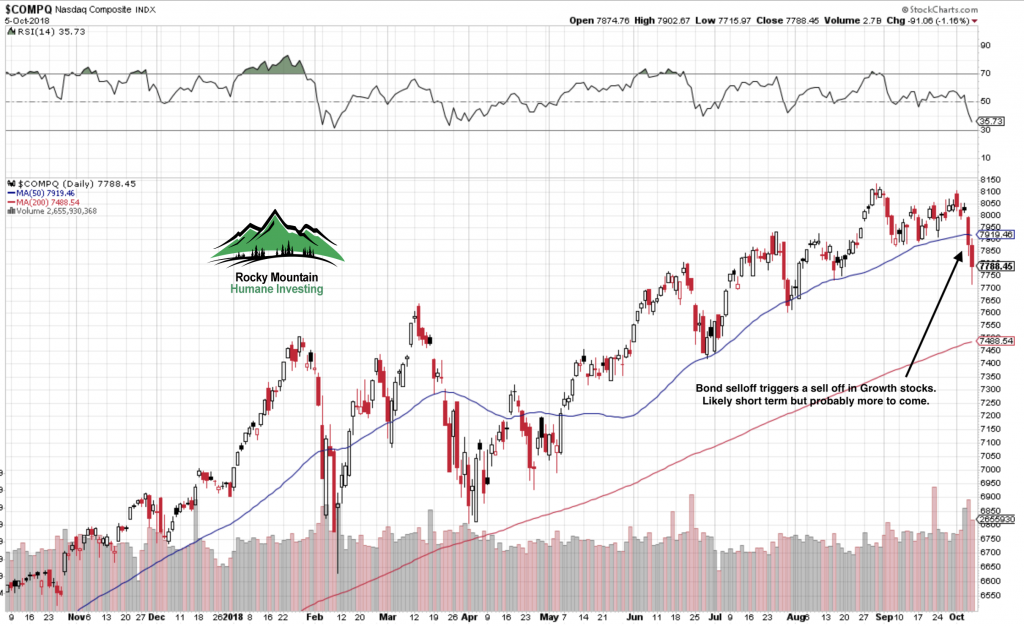

My guess is that the selling is not finished. We may bounce here for a day or two, but if the bond market continues to be weak, the Nasdaq Composite (Chart 5) could visit 7500 or so quickly. Selling would likely be contained at that level. Odds are high this is not the start of a bear market for stocks.

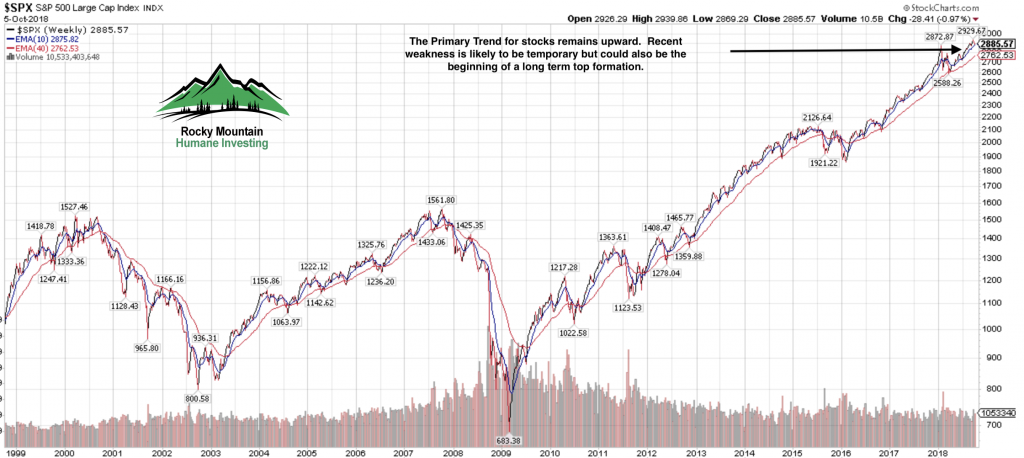

Chart 6: Our long term primary trend indicator remains quite positive at present. Market tops are usually made by a rolling-over process rather than a mountain top peak. See my estimates for business cycle – stock market peak below.

Parlor game guesses for cycle peaks

Based on the Fed’s rate hike projections, we’ll reach inversion by February 2019. The Fed has given no signal to indicate they’ll declare a halt to rate hikes which could push the date to later next year. In fact the most recent jobs data makes me think they’ll hit the brakes hard next year.

So, based on an inversion in February 2019 we can make some recession date assumptions based on the past 9 yield curve inversions dating back to 1957:

The shortest lead time from inversion to recession has been 8 months: October 2019. Median lead time from inversion to recession has been 12 months: February 2020.

Longest lead time from inversion to recession has been 20 months: October 2020.

Understand the recession data is based on NBER declared recessions and they date the start of a recession many months in hindsight. But we can make reasonable estimates based on yield curve inversion dates.

The stock market is a forward looking barometer meaning that the markets look ahead into the future. This means the US stock market will peak and begin to rollover before the recession starts.

Based upon data from 1957, the US stock market has peaked on average 5 months before the start of a recession.

Earliest estimated stock market peak is May 2019. Likeliest estimated stock market peak is September 2019. Latest estimated stock market peak is May 2020.

Thanks again to all of you for your trust. As an investment manager, my goal is to avoid the dogmatic approach, be flexible and neutral to market behavior. Any investor who decides to get into an argument and mansplain to the market will emerged bruised and poorer for the experience.

Recently I’ve seen a few studies and charts on Twitter that lend favor to Tax Efficient Investing. These are portfolios where each holding is designed to be held for more than one year. This stragegy allows them to qualify for reduced taxes as a Long Term Capital Gain. The articles I’ve seen generally advocated by financial planners and advisors who see Tax Efficient Investing as their way to add value or have an edge for the clients of their practice. But not once have I seen a credible article playing the role of Devil’s Advocate for Tax Efficient Portfolios. Today the Dow Jones Index was down 660 points at mid-day. It would seem apropos to highlight a few of the disadvantages of Tax Efficient Investing.

The points I will make are from the perspective of a Growth-oriented investment advisor whose primary investment vehicles are stocks, ETF’s and ETN’s. Municipal bonds are a different animal altogether and not the subject of this blog post.

Are the lower taxes worth the losses?

The primary objective of Tax Efficient Investing is to own an investment for at least 12 months. Our primary objection to this strategyis prioritizing time of ownership over gains. Investment gains can disappear or be significantly reduced by the goal of hanging on for one year. For example, you buy a stock at $50 on January 1, 2017 and perhaps by April 2017 the stock is $65. But by January 2, 2018 the stock could be anywhere. A major sin of investing that you open yourself up to is not taking the gain in April. If the market goes into a sell-off where the stock goes back to $50 or below, your gain has been negated. It reminds me a bit of the game show “Let’s Make A Deal” with Monty Hall. Monty would offer a contestant a sure deal right off the bat, but with the caveat of “Would you be willing to give up the sure deal for whats behind Door 1”. It could be a brand new living room or dinette set (hey I watched it in the 1970’s). It could also be a rusting bucket of used auto parts. At that point Monty would offer the bizarrely dressed contestant the consolation prize of the home version of the game show. Cue sad trombone.

The stock could also have gone to $75 in good market as well, up 50%. If the stock continues to rise without any major setbacks, an experienced Trend Following methodology as well as a Tax Efficient investor would likely continue holding on to the stock. There is a primary difference between a Trend Following system – which we employ – versus a Tax Efficient strategy. We’d take a profit should the stock decline below important benchmarks. Declines below certain sell points raise the question of whether the stock is even in an uptrend. By the way, how hard it is to find a stock that can smoothly rise throughout the entire year? This means the company must produce 4 good earnings reports in a row and not sustain large pullback. 2017 was an easy year for Trend Followers. Even then almost 95% of the stocks we bought could not sustain 12 months of positive performance.

Are the drawdowns tolerable?

In point 1 I discuss a scenario of a single stock. But if Tax Efficiency is the goal along with long term Growth, you can now envision how volatile that portfolio would become. By not exerting proper risk controls, the portfolio would likely have longer and more significant drawdowns. Is that something you really want? Most investors, especially those who are new to investing cannot endure declines of 30% or more to their portfolios. This begs to ask: “Would you pay a bit more in taxes for less volatility?” In my experience which is based on client retention, the answer is “yes”. People hate losing money more than paying higher taxes.

What about lagging holdings?

Digging down deeper into portfolio management is the issue of what to do with lagging holdings. A lagging holding is the stock that you have had a gain on, but is now going nowhere. Our view is to sell laggards in a rising market. We don’t see the value of holding an investment unless its producing for you. A major advantage to this is to look for new potential winners. But the Tax Efficient portfolio may hang on to the stock till it clears the one-year hurdle. This is another factor contributing to underperforming portfolios.

To sum it up: Tax Efficient Investing can be a proper strategy for some investors but for most it isn’t. Investment methods must not just make financial sense. The methods must also be cognizant of the investor’s risk profile and emotional impact. One size does not fit all and every investment method has some inherent weaknesses. Most investors would probably feel more comfortable knowing the achilles heel of any strategy.

We are taking the profit in shares of SGOC after the stock erupted for another 35%+ gain this morning. Stocks that go parabolic usually become very unstable when profit taking eventually takes over and we’d like to be out of the stock before that begins to happen. As you can see by the chart it has made similar leaps before but it usually gives up about half the gain in short order.