The Post Parabolic Blues

4/8/2018

Since the 10% decline in the S&P 500 index in late January I’ve been using my Bull Market playbook to deal with a decline. Technically speaking we are still in a Bull Market but our Bull status is looking more precarious by the day. The Bull Market playbook means I’m looking for a double bottom or retest of the market lows off the initial sell-off. Secondly, I’d be looking to buy stocks on signs of a successful retest and rally.

Friday’s 2.19% decline was especially disheartening since it wiped out three days of gains. Stocks had been showing signs of recovery by trying to build a base from which to rally. Previously, markets were appeased by the story that the White House was using the tariff threats as a negotiating tool. But Friday’s news showed that markets are not buying that story any more. This is a dangerous and unpredictable situation that leaves any investor unhedged in stocks vulnerable to policy mistakes and reckless statements from the White House or cabinet.

The second leg down rallies have been relatively weak with reduced volume while declines have been larger in magnitude and increased volume (not good). This reveals that large institutional investors are in a liquidation mode and are using rallies to sell rather than using declines to accumulate. This is Bear Market behavior and is giving me pause to reassess the likelihood of another another significant leg down for stocks and the possibility of a Bear Market.

Perhaps this weakness is the aftermath of the parabolic rise in stocks earlier this year? Plus the extreme readings of investor sentiment? It’s possible, but I’d argue that stocks and bonds are now reacting accordingly to an aggressive Federal Reserve and a much higher than average possibility of policy mistakes from the White House.

Chart 1

Chart 1 above, courtesy of Carl Swenlin of Decisionpoint, shows the importance of the $257 level for the “SPY” aka S&P 500 ETF. Both the 200 day moving average and the underlying trend line from the 2016 rally converge at nearly the same level.

There are also other important issues the world stock markets are contending with:

The global economic recovery is mature and slowing. Worldwide GDP data is showing clear signs of slowing.

Policy Errors: The tax cuts are the personification of fiscal irresponsibility and there’s no going back.

Trade Wars are “good and easy to win”. Investors aren’t fooled in the least by this rhetoric (see Smoot-Hawley Tariff Act). We’ve never had a President who can just as easily talk up a stock market and talk it down with rhetoric within weeks. This is certainly a market headwind for stocks.

Chart 2

Aggressive Federal Reserve: The “Yield Curve” (shown above in Chart 2) is growing increasingly negative as short term interest rates are rising which will eventually kill the economic expansion. This causes investors to buy long term Treasury bonds. The higher short term yields and lower long term yield flatten the difference between short and long term rates which reduces the incentive for banks to lend.

The Yield Curve is a simple indicator and one of the most powerful tools to predict markets and the economy. Once the curve drops to .5 its “Goodnight Irene” for stocks and “Good Day Sunshine” for Treasury bonds. This is why we’ve recently added long term Treasury bonds to client portfolios.

If you’d like to learn more about the Yield Curve, there is an array of data from none other than the Federal Reserve:

https://www.clevelandfed.org/our-research/indicators-and-data/yield-curve- and-gdp-growth.aspx

Our Present Status: A sharp break in the price in Chart 1 below $257 without a rebound implies there is more selling ahead, which could be significant. Since my style of investing is based on reacting rather than predicting, I’d look for a $257 break to increase our existing hedges and further reduce stock holdings.

Should the price break below $257 not occur or occur briefly, I’d keep the status quo but expect the bottoming process to take longer than expected. I’d likely prefer to reduce stock holdings in strength until we see a positive change in market behavior.

Treasury bonds: My W.A.G. for Treasury Bonds and the economy is that the Yield Curve inverts in 2019 which will cause a full blown bear market in stocks and bull market in Treasury bonds. T-bonds could rally by more than 20% due to the reduced effect of lowering interest rates in an already low rate environment by the Fed. This could be followed by recession and bear market low by 2020.

Bottom Line: I’m agnostic to market direction as we can generate profits in accounts regardless of market trends. It’s the transition periods which we are possibly in that are tricky to assess. Once a new trend emerges, be it up or down, I’ll adapt and do my best to continue generating profits on your behalf.

Thank you,

Brad Pappas

Enjoy The Ride!

10/19/2017

Since the market bottom last November the S&P 500 has rallied from 2083 to 2560, a very healthy gain of 22.8% not including dividends. Despite these gains there are almost no signs of euphoria within the investing community which leads me to think this rally still has a long way to go. Euphoria is a necessary evil that’s almost always seen at major market highs when investors refuse to believe the market will roll over.

Is there a valid case to be Bearish? Yes, but market momentum always takes precedence. Eventually the bears will be right but it may take a few more years and in the meantime so much opportunity will be lost. The bearish arguments have been around for years and completely dismissed as markets make new The bear case always sounds intelligent and well thought out but their losses and opportunities missed can be staggering.

This week marks the 17th time in the past 90 years that stocks made new all-time highs each day of the week. In only ONE instance did this ever mark the exact top of the stock market (1968). Higher highs occurred 94% of the time.

Once a trend has been established it tends to persist and run its full course.

Investing always has some form of anxiety for investors to contend with. If it’s not nervousness with the decline in your account value it’s the fear of the value rising too much and worrying you’ll give it all back. Is there a Goldilocks too hot – too cold – just right equivalence? Nope, but keep things simple as in try to sensibly grow your principal as much as possible in the good years and lose as little as possible in the bad. And, try not to mess it up in the meantime which is why: Temperament can more important than intellect.

In past years bonds offered a decent yield which allowed an investor to gain some income and diversify from stocks. The problem in this era is that yields are very low and in order to gain a modest, even a high single digit return there must be some increase in bond prices and very little of that is happening now.

One of the best books ever written on investing was authored by Jesse Livermore “How to trade in stocks” published in 1940. At his peak Livermore was worth an estimated $100 million in 1929 dollars after starting from scratch. His approach was systematic and still effective today and I use many of the rules he originally created for himself.

One of Livermore’s lessons was: “Money is made by SITTING not trading” To paraphrase, when you know you’re in the right you stay invested until the rally fades. You should remain in the stocks that are trending higher and take small losses along the way (never ride a losing stock down hoping it will turn).

The majority of “easy” money made in stocks is made during two unique phases of the economy/markets: The violent rally higher during the transition from recession to expansion and during long trending rallies in the mid cycle of the expansion like we’re experiencing right now. Smooth trending markets may happen just once or twice in a decade so it’s important to maximize the opportunity when it’s present.

While it’s part of our management philosophy to protect our clients during major down drafts, we do not sell prematurely or pretend that we can call a market top. “Top Calling” the stock market is a way of gaining media exposure and attention. Top Calling has nothing to do with solid investment management since astute advisors know it can’t be done. The better option is to let the market take us out when the time is right with our built in exposure systems.

Charting the warning signs of the 1987 crash

It’s been 30 years since the 1987 crash so why not look at it closely for lessons?

The evolution of market tops is a gradual process whereby markets weaken as selling and distribution increase. Sometimes the flat sideways trend is nothing more than the “pause that refreshes” before another up-leg commences. However, sideways/choppy trends can also be the early stage of something more ominous.

In the summer of ‘87, the bond market was very weak with declining prices and higher yields which were becoming increasingly more attractive to stocks. This was causing a migration from stocks which began to manifest itself in August. These were the grand old days when investors wouldn’t buy a municipal bond unless it had a tax free yield of 10% or more.

Stocks peaked in August then sold off by 8% in September then rallied 6% into October before crashing. The decline in early October breached the 50-100-200 day moving averages which would have triggered a wave of sell signals for us. We always use the 200 day moving average as the ultimate cut off for owning stocks. I consider declines below the 200 day to be Bear Market country.

Summary: Enjoy the ride.

Brad Pappas

970-222-2592

Brad@greeninvestment.com

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision. All expressions of opinion are subject to change without notice in reaction to shifting market, economic or political conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed. Past performance is no guarantee of future results.

Like so many other investment firms we had to endure the market decline in 2008 but being an independent firm we have the freedom to also say “never again”. We’ve reached a point in our lives and stomach lining that there had to be precedents before the recession that could provide a heads up if a recession is looming. In fact, over the years we’ve found many including Inverted Yield Curves written none other than the Federal Reserve.

One thing you’ll notice over time with our blogs or letters is that we’re not opposed to using the research of other firms especially if they blend nicely with our own systems. We have often relied on academic research of others to build upon and couldn’t care less if research results were developed by others. We always find it a bit small minded that so many firms insist on relying solely on their own research or incredulous when studies that could really help their clients are ignored. Why reinvest the wheel if its already been done by someone else?

Our priority is to develop effective systems which deliver superior results to our clients and not claim that we have a monopoly on great ideas. We have just a few criteria’s that must be met for inclusion to our own systems. System should be open (no black boxes) and understandable and best of all, relatively simple. Too many times we look at systems of others that have done a remarkable job in back testing but when you look at the system details there’s a large number of criteria which just makes us think the system has been optimized to inevitable failure.

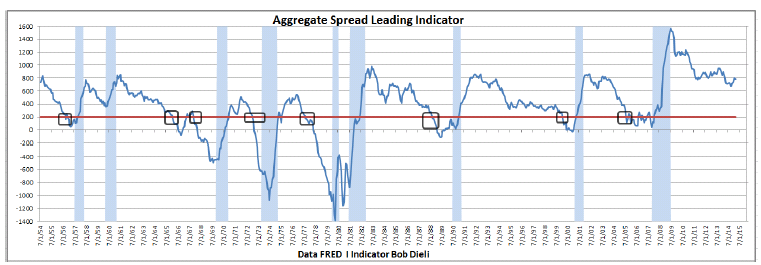

Things brings me back to Bob Dieli of www.nospinforecast.com

Decades ago Bob developed the Aggregate Spread as a leading indicator of US recessions. The formula is absurdly simple for those inclined: Take the 30-year Treasury bond yield and subtract the yield from the Fed Funds rate. And then take the CPI rate and subtract that from the unemployment rate. Then just subtract the yield spread from the result of the CPI minus the unemployment rate. That will give you the Aggregate Spread.

When the Agg Spread dips below 200 the odds become very high that a recession is expected in the next 9 months. Simply put to you the investor: If you have high probability of advance knowledge of an incoming recession why would you want to own stocks or own stocks un-hedged?

One of the great things about Bob’s Agg Spread methodology is that it goes back a long ways, back to the days of Elvis, 1954. Bob has been operating the system since the early 1980’s. During this time the system algorithm has never been changed either.

While the Agg Spread is not a guarantee of a recession or the ensuing Bear Market in stocks that could cause investors to lose 20% to 40+%. Using the Agg Spread places the investor into a position of preemptive rather than reactive. With this type of knowledge investors can have an advanced warning to move at least a portion of their assets out of stocks and into short term Treasuries or hedge the portion of the portfolio close to 1 to 1 that closely correlates to the S&P 500 with the symbol “SH“.

Brad Pappas

No Positions

Advisers who tell their clients to remain fully invested in stocks, hell or high water is offering systemically dangerous advice. @Jesse_Livermore

We couldn’t agree more!

But we live and work in Lyons Colorado, so “high water” is a poorly timed phrase.

As a private investment management firm we’re not restrained from reducing risk when we see fit. Perhaps its an old Irish Catholic bromide that “No good will come of this” attitude rears its head every time I see and excessive or parabolic moves in markets, asset classes or stocks. Parabolic Markets = The End is Near.

We’ve seen these kind of parabolic moves before: Treasury Bonds in 2012, Gold in 2011, the NASDAQ in 2000-2001. In 2013 we took profits in parabolic stocks such as FU, SGOC, FONR. All three gave back their gains and in the case of FU – the company has been delisted with balance sheet issues.

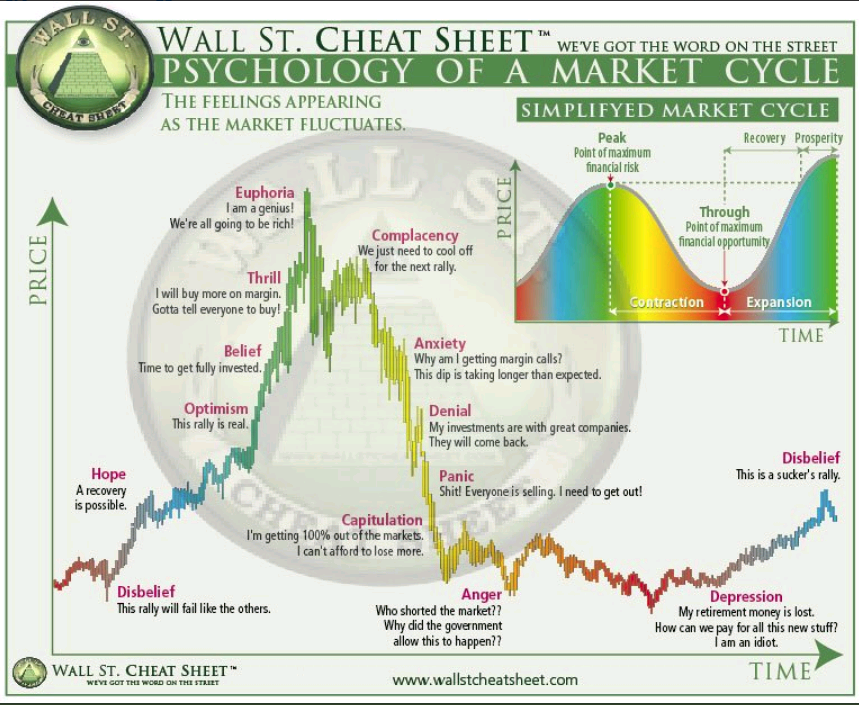

Do you remember 1987? Big hair and even bigger shoulder pads. Celtics and Lakers along with team oriented basketball. Duran Duran and endless amounts of Phil Collins and a parabolic stock market that never pulled back until the music ended on October 19th where the Dow Jones Industrial Average dropped 22.6% in a single day.

Some but not all of the main culprits of the crash are evident now and while market cycles never entirely repeat themselves, they can echo the movements of the past. I believe there is a good chance that we’ll see a short and sharp market sell off sometime soon to alleviate the extreme investor bullish psychology.

What the markets have going for themselves for the time being is a nil chance for a recession anytime soon. Most major Bear Markets occurs as the economy is heading into recession and that is not the case. So, what I’m expecting is a brief but potentially painful market correction of short duration that could commence at any time.

Most market pullbacks can largely be ignored as we can’t compensate for all of them. My focus is to identify the environments where major pullbacks are likely. Pullbacks of the size that they cannot be ignored, in the range of 20% to 30% or more.

The biggest hurdle for the markets going forward is the issue of extreme investor bullish sentiment. For those unaware, “sentiment” is an inverse indicator. This means when investors (both pro’s and amateurs) are extremely bullish its a negative and high risk for the markets. When those investors are extremely negative its a positive and low risk environment for stocks.

I recently came across a very good paper discussing the relationship between sentiment and stock returns: “Investor Sentiment and The Cross Section of Stock Returns” by Malcolm Baker and Jeffrey Wurgler. Published by National Bureau of Economic Research.

Page 5: “When sentiment is low (investors are bearish) subsequent returns are higher on young stocks than older stocks, high return volatility than low-return volatility stocks, unprofitable stocks than profitable ones, and non payers rather than dividend payers. When sentiment is high (as it is now), these patterns completely reverse. In other words, several characteristics that were not known to have and do not have any unconditional predictive power actually reveal sign-flip patterns, in the predicted directions when one conditions on sentiment.”

In plain English, this means that the stocks that were so profitable for us when investors were fearful and negative can turn quickly and decline sharply in price when investors are too giddy and positive.

The chart below will give you an idea of how extreme sentiment is at present and where it ranks in years past, and a look to what happened going forward. Remembering the “echo” Investors Intelligence Bulls minus Bear is the highest since February 1987.

But what contributed to this extreme positive sentiment? Here are some culprits:

But what contributed to this extreme positive sentiment? Here are some culprits:

2013 was the first time since 1995 where the S&P 500 Index never declined to touch its 200-day moving average.

So as of the end of the year the S&P 500 would have to decline at minimum 10% to even touch the present 200-day moving average. This also means that select portfolios with less than 500 stocks would likely fall greater than 10%, 20% would not be surprising.

In December the Federal Reserve announced they will be “tapering” Quantitative Easing. The chart below shows the previous attempts to wean the economy off of QE and subsequent market reaction. Note: Once difference to this round of tapering is that the economy is not quite as weak as before which may account for no immediate market sell off.

Lastly, we have the Presidential Cycle. The Presidential Cycle is a way of looking at the equity markets through the lens of 4 year Presidential term. The Presidential Cycle is closely related to the business cycle which is largely controlled by the Federal Reserve. The second year of the Presidential term is uncharacteristically weak relative to the other three years. Don’t let the mean rate of return fool you, there have been many second years where at some point the major market indices were down in excess of 10%.

Not since 1995 has the S&P 500 not had at least a 10% pullback. Normally, you can count on a 10% pullback within an ongoing bull market to a great time to add funds or bring new accounts online. But 2013 is the year of the relentless rally where 2% pullbacks are new 5% pullback. Extreme bullish investor sentiment which is normally a good barometer of when to ease up on portfolio exposure has been pointless, as previous blog posts have demonstrated.

So, whats going on you ask? Why is this year different from the others and what does it mean going forward?

Markets are clearly being driven higher by the Federal Reserve current policy of Quantitative Easement and its by product of 0% short term interest rates.

Its no coincidence that when the Fed ended QE1 and QE2 markets fell apart with declines of -16% and -19% respectively in 2010 and 2011.

Its fashionable right now to analyze each economic tick (especially the recent positive employment data) to determine when the Fed will end QE3. But the truth is we really don’t have an accurate guess for when that will happen.

Three things we know for sure at the moment:

1. We are in the midst of the strong season for equities and that will last until March 2014.

2. The economy as measured by employment is improving. Contrary to politically biased media outlets job growth is not coming from part time employment. GDP growth in the 3rd quarter was stronger than expected. This is market friendly.

3. Bob Dieli’s Aggregate Spread and RecessionAlert.com are both at benign/miniscule odds of recession. Market friendly again.

My best guess of what will happen? Eventually the Fed must end QE3 and the markets may anticipate this ahead of time by churning nowhere or showing internal deterioration in strength. My thinking is that the Fed will do nothing till at least after congressional budget talks in January but by the time March comes around and temps here begin to melt some snow we should be decreasing our equity exposure in a meaningful way.